How Urban Land Became a Global Extraction Machine

World Urban Forum 13 in Baku has come to a close. Here some takeaways in the form of a longer essay about cities and their complex relationship with one of the predominant land uses: housing – particularly of the affordable type.

The forum used the language of urgency. Delegates spoke about affordability, resilience, inclusion, displacement, and the right to housing. The official Call to Action acknowledged that the global housing crisis is rooted in “deep structural, systemic, and governance failures.” It named speculation, commodification, weak land governance, shrinking public investment, and the increasing financialization of housing itself. That language matters because for decades global housing debates have hidden behind technical vocabulary designed to avoid political confrontation. Governments talk about supply shortages, permitting delays, demographic pressure, or construction productivity. Developers complain about regulation. Economists debate elasticity. International institutions produce targets, indicators, declarations, and frameworks. Yet beneath the technical language lies a far more uncomfortable reality: The global housing crisis is fundamentally a land crisis. More precisely, it is a crisis produced by the transformation of urban land into one of the largest extraction mechanisms in modern capitalism. This is what contemporary urban discourse still struggles to confront honestly.

The problem is not simply that cities failed to build enough homes. Many cities built enormous amounts of housing. Towers rise across skylines everywhere from London to Shenzhen. Construction cranes dominate urban horizons. Entire districts are continuously redeveloped. Yet affordability keeps collapsing because the issue is not merely the quantity of buildings. It is the financial logic governing the land underneath them.

Take a journey. Not a comfortable one.

Take Nairobi’s Kibera, the largest informal settlement in sub-Saharan Africa, where somewhere between 200,000 and 700,000 people live depending on whose estimate you trust. The uncertainty itself says something. Corrugated iron roofs stretch endlessly across muddy pathways. Entire families live in single rooms of perhaps twelve square metres. Water is expensive. Electricity is dangerous and often illegal. Sanitation infrastructure is grossly inadequate. Yet Kibera persists because it performs an urban function formal systems increasingly fail to provide: access to the city at a price poor households can still partially afford.

Or take Dharavi in Mumbai, often described as Asia’s largest informal settlement. Around one million people live within little more than two square kilometres. Outsiders routinely describe Dharavi as urban failure. Yet Dharavi is also one of the most economically productive districts in Mumbai. Recycling industries, pottery workshops, textile production, food systems, tailoring, logistics, and small manufacturing all operate within an extraordinarily dense urban ecosystem. For decades governments and developers have attempted to “redevelop” Dharavi into formal high-rise housing. But many residents resist these plans because they understand something technocratic housing policy repeatedly ignores: housing separated from livelihoods, transport, customers, social networks, and economic geography is not equivalent housing. Relocation often means impoverishment.

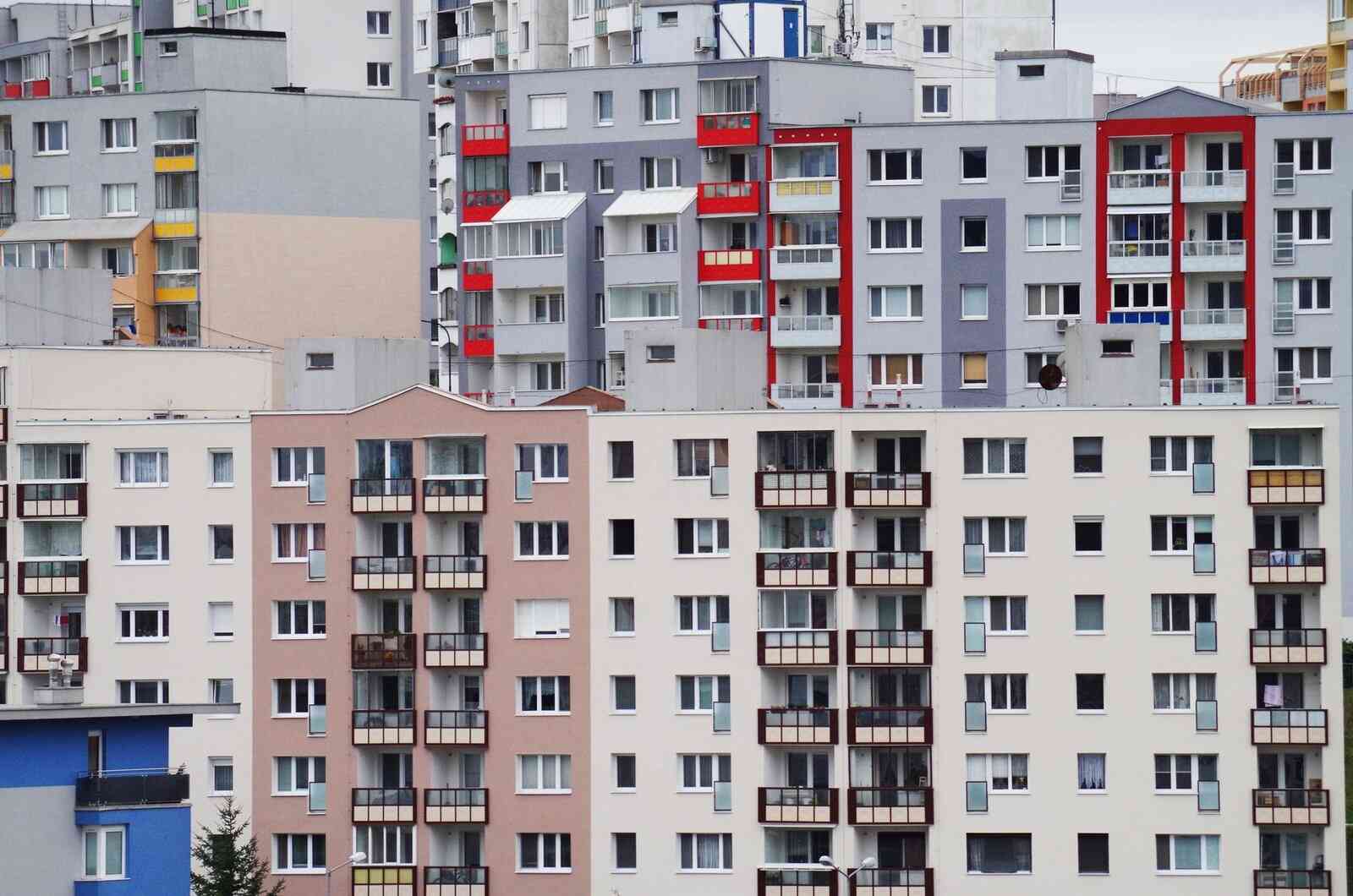

The same contradiction appears in Shenzhen. Forty years ago Shenzhen was a city of about 100,000 people. Today it contains more than seventeen million inhabitants. The speed of urbanization produced forests of towers alongside dense “urban villages,” former rural settlements absorbed into the expanding metropolis. These villages became affordable entry points for migrant workers because they provided access to urban opportunity. Over time many were demolished in the name of modernization and land valorization. What disappeared is not merely cheap housing. It is affordable urban access itself.

Hong Kong represents perhaps the purest expression of the crisis. More than 220,000 people live in subdivided units, some barely large enough for a mattress. “Coffin homes” became a global symbol of urban dysfunction not because Hong Kong lacks housing towers, but because one of the wealthiest cities on earth organized its land system almost entirely around scarcity and asset inflation. Housing prices rose to more than twenty times median annual household income.

The perversity of the system becomes clearer once one realizes these outcomes are not market failures according to the prevailing logic of urban development. They are successes. Rising land values strengthen municipal balance sheets. They increase tax revenues. They attract global investment. They stabilize political coalitions built around property ownership. Pension funds depend on real estate appreciation. Banks depend on mortgage growth. Governments quietly rely on housing inflation to compensate for stagnating wages and weak productivity growth elsewhere in the economy.

Cities increasingly depend financially on unaffordability – the contradiction sitting quietly underneath almost every housing debate.

Amsterdam reveals the transformation especially clearly because it was historically regarded as one of Europe’s most socially balanced housing systems. For much of the twentieth century housing functioned largely as infrastructure. Large-scale social housing, public land management, and regulated development kept the city relatively accessible across income groups. Then the financial era and a market-liberal government arrived. Cheap global capital, ultra-low interest rates, constrained supply, and the political sanctification of property ownership fundamentally changed the city’s land market. Housing ceased functioning primarily as shelter and became a global financial asset. Apartments in central Amsterdam increasingly detached from local incomes altogether. Today a two-bedroom apartment can easily cost around 600,000 euros and more while social housing waiting lists stretch beyond fifteen years. Teachers, nurses, young professionals, and public-sector workers increasingly struggle to remain inside the city they sustain and are forced out. What happened in Amsterdam matters because it demonstrates that even highly competent, well-governed cities become unstable once urban land becomes globally financialized.

London followed a similar trajectory but at much larger scale. Median house prices now stand at roughly eleven times median annual salaries. More than 100,000 households live in temporary accommodation. Entire districts have been transformed into investment landscapes where apartments are purchased not primarily for occupation but for capital preservation. The skyline itself reveals the logic physically. Luxury towers rise around transport hubs and former industrial land. Units are marketed internationally before construction even begins. Some remain largely dark at night because they function less as homes than as financial instruments. Urban planning, which once claimed to organize collective development, increasingly functions as a mechanism for producing land value.

San Francisco pushes the contradiction even further. One of the richest urban economies in human history simultaneously contains mass homelessness and extreme housing scarcity. Roughly seventy percent of residential land remains protected by low-density zoning while rents climb beyond the reach of ordinary workers. Again, from the perspective of landowners, this is not failure. Scarcity protects value.

Housing as an asset or housing as a basic human right?

This is why the dominant housing discourse increasingly feels detached from reality. Build more housing. Relax zoning. Speed up permits. Streamline approvals. Increase supply. Certainly more housing is needed in many places. But supply alone cannot solve a system where urban land itself operates primarily as a speculative financial asset. Under financialized conditions, new supply is often absorbed directly into investment markets. Construction booms coexist comfortably alongside worsening affordability. The problem is deeper than construction. Housing affordability is fundamentally land affordability.

Buildings deteriorate. Concrete cracks. Roofs leak. Pipes corrode. What appreciates is land. And urban land appreciates because cities concentrate value: jobs, infrastructure, mobility, education, public investment, culture, safety, and economic opportunity. That value is collectively produced. Yet most of it is privately captured.

The economist Joseph Stiglitz has argued that much of the wealth growth in advanced economies over recent decades came not from productive investment but from rising land values. The numbers are striking. In the United Kingdom, residential land values increased roughly 450 percent in real terms between 1995 and 2022. In Australia, land now accounts for around two-thirds of total residential property value compared with roughly one-third in the 1970s. In the United States, housing costs have risen roughly three times faster than incomes since 1960. This is not merely a housing problem. It is a land extraction system. And the public sector is deeply implicated in it.

One of the least discussed realities at the World Urban Forum was the extent to which governments themselves now depend on speculative land inflation. Municipalities sell public land because they need revenue. Infrastructure projects are justified partly through anticipated land value uplift. Planning systems often manufacture scarcity because scarcity generates fiscal value. Political systems increasingly protect homeowners because housing inflation has become the primary mechanism through which middle classes accumulate wealth.

The same governments that publicly lament unaffordability are financially dependent on its continuation.

This creates an extraordinary contradiction at the heart of contemporary urban governance. Cities simultaneously promise affordability while structurally depending on rising land prices. The result is a kind of institutional schizophrenia. Housing is described publicly as a human right while urban policy quietly treats it as an investment class.

The uncomfortable truth is that contemporary urbanization increasingly depends on exclusion. Cities require low-wage workers to function, yet rising land values systematically expel them. Teachers, cleaners, nurses, transport workers, delivery drivers, service employees, and young families become economically necessary but spatially disposable populations. They are pushed outward into longer commutes, overcrowded housing, peripheral settlements, or informality. Meanwhile governments continue describing rising property values as evidence of urban success. This ideological inversion may be one of the most destructive features of contemporary urbanism. Cities have become so dominated by asset logic that affordability itself increasingly appears economically suspicious.

Vienna remains one of the few major counterexamples. Around sixty percent of residents live in subsidized or limited-profit housing. The city maintained strategic public land ownership over generations and treated housing as long-term civic infrastructure rather than purely as a commodity market.

Singapore represents another alternative, though through a much more centralized political system. Roughly eighty percent of residents live in Housing Development Board (HDB) housing built on publicly controlled land. The HDB system combines state land ownership, long-term leaseholds, regulated resale structures, and coordinated planning. Whatever one thinks of Singapore politically, it demonstrates that governments can shape land markets decisively when they choose to do so.

Tokyo offers another lesson entirely. Unlike many Western cities, Tokyo allowed relatively continuous urban densification over decades. Scarcity remained less politically manufactured, which moderated speculative pressure. Tokyo is expensive, certainly, but it largely avoided the catastrophic detachment between land values and ordinary urban life seen elsewhere.

These examples matter because they expose one of the great myths of contemporary housing discourse: that current outcomes are inevitable consequences of population growth or anonymous market forces. They are not inevitable. They are political. And increasingly they are produced deliberately.

Common land as commons

A genuinely serious response would therefore require confronting urban land directly. Not merely regulating development more efficiently. Not simply subsidizing first-time buyers. Not just accelerating permits. It would require reducing the role of land as a speculative wealth-generation mechanism.

Here some suggestions:

Municipal Land Trust: One possibility would involve municipal land trust exchanges in which strategic urban land gradually transitions into city-managed trusts. Existing landowners would not simply lose their property through expropriation. Instead, they would receive stable dividend-bearing shares linked to inflation and moderate metropolitan growth rather than speculative escalation.

Urban Sovereign Wealth Fund: Another model would create urban sovereign wealth funds. Instead of continuously selling public land to close fiscal gaps, cities would retain ownership, lease development rights, recycle revenues into new acquisitions, and slowly build permanent metropolitan land portfolios.

Dynamic Land Value Corridor: Cities could also establish dynamic land value corridors in which excessive land inflation automatically triggers anti-speculation measures, vacancy penalties, escalating taxes, or public value capture mechanisms.

Property Rights Separation: Property rights themselves could be partially unbundled. Occupancy rights, inheritance rights, development rights, and speculative resale rights do not necessarily need to remain fused together permanently. People could retain secure housing and moderate wealth preservation without every parcel operating primarily as an extraction mechanism.

Commons Transition Zone: Metropolitan commons transition zones could gradually move land toward shared stewardship over generations through inheritance, rezoning, or redevelopment mechanisms.

None of these ideas abolish markets or eliminate private property. What they attempt instead is something more subtle and perhaps more realistic: reducing the degree to which urban land functions as a speculative asset disconnected from urban society itself. And this is ultimately where the World Urban Forum revealed its deepest contradiction.

WUF13 proudly celebrated record participation, with roughly 39,000 registrations. The scale of the event was undeniably impressive, and the Azerbaijani hosts deserve genuine recognition. The hospitality extended to participants was remarkable, and the logistical organization of a gathering of this size was exceptionally professional. Yet the symbolism of the record attendance also revealed something uncomfortable about contemporary global urbanism itself. Urban policy increasingly risks becoming performative in much the same way urban development has become performative. Bigger summits, larger delegations, more declarations, more frameworks, and more carefully branded commitments all create the appearance of accelerating action while the underlying structures driving the crisis remain fundamentally intact.

After decades of urban forums, housing strategies, sustainability agendas, investment conferences, and affordability pledges, the basic trajectory of urban land markets has barely changed – rather the contrary happened: In many cities it has worsened dramatically. At times the global urban policy circuit risks resembling the speculative urbanism it claims to critique: highly networked, optimistic in language, internationally mobile, rich in branding and visibility, but often disconnected from the structural political reforms required to alter urban reality itself.

The housing crisis therefore reveals something larger than housing. It reveals a civilization increasingly unable to distinguish between economic value and social value. A city where ordinary people cannot afford to live is routinely described as economically successful. A city where teachers commute three hours daily is considered globally competitive. A city where housing functions primarily as an investment vehicle is treated as financially healthy. This is not merely a policy failure. It is a moral failure embedded directly into the structure of contemporary urban capitalism.

And that is the uncomfortable implication still hovering beneath almost every global urban discussion, including those in Baku. If housing insecurity is rooted in the financialization of urban land, then solving the crisis ultimately requires limiting the power of land markets themselves, which means confronting one of the central accumulation systems of the twenty-first-century global economy.

The scale and magnitude of the changes needed are precisely why governments prefer talking endlessly about affordability while allowing the crisis to deepen year after year.

cover image: https://pxhere.com/en/photo/1323967